UPDATED: Foreign Investors Scale Back H1 2025 Dealmaking

Foreign VC first investments dropped to 49% of total deals, breaking the 60% historical average maintained from 2016-2024.

Welcome to Israel Tech Insider. I’m Amir Mizroch, a tech communications advisor and former EMEA Tech Editor at The Wall Street Journal. This newsletter is about connecting the dots to give you a sharp, insider’s take on what’s really going on in Israel’s tech industry.

As always, feedback to amir@israeltechinsider.com

Note: This article has been substantially revised following investor feedback that clarified the distinction between deal sheet visibility and actual investment activity, correcting the initial mischaracterization of foreign investor behavior as an "exodus" when evidence suggests continued engagement through larger, longer-stealth funding rounds.

An earlier version of this post said that foreign investor activity in Israeli tech has cratered to historically low levels, with established players like Index Ventures and Andreessen Horowitz completely absent from H1 2025 deal sheets.

But thanks to a smart investor friend, I’m humbly able to say that the picture is a more nuanced than I previously thought. H1 2025 data from the new IVC-GNY-KPMG report suggests foreign investor exodus—but the mechanisms of how this industry works reveal a more complex recalibration of risk, timing, and stealth capital deployment that challenges my initial surface-level panic narrative.

Foreign VC first investments indeed dropped to 49% of total deals, breaking the 60% historical average maintained from 2016-2024. Yet this metric captures disclosure moments, not funding decisions. While there are fewer of them, the early-stage rounds that have taken place have been dramatically bigger, allowing startups to extend stealth phases without immediate follow-on pressure.

And while Andreessen Horowitz and Index Ventures did not, as of the IVC report release, show up in H1 deal sheets, A16Z has in fact organized Israeli founder events during the summer. It apparently even caught flack on line for that.

Corporate venture capital presents the clearest retreat signal. Foreign corporate VC first investments crashed from 44 deals in 2022 to 4 in H1 2025. But context matters: Samsung Next and Verizon Ventures shuttered failing Israeli operations years ago, preferring centralized corporate venture strategies over dedicated local presence. Their absence reflects operational efficiency, not geopolitical flight.

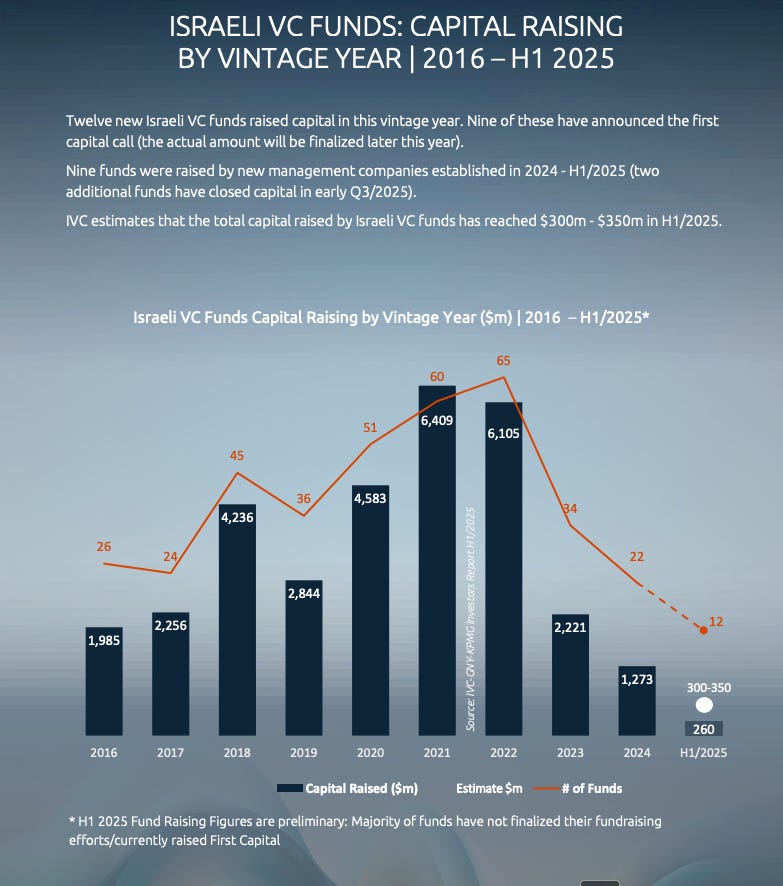

Domestic funding shows genuine stress signals. Israeli institutional investors directed 79% of their $87 million toward follow-ons rather than new ventures—a defensive posture that prioritizes portfolio preservation over ecosystem expansion. Twelve new Israeli VC funds raised a modest $260 million in H1 2025, projecting toward a 60% annual decline from 2024's already-compressed $1.27 billion.

Investment concentration reveals strategic prioritization. Generative AI leads all sectors, while cybersecurity attracts "enormous sums"—Cato Networks' $239 million round and Sentra's $50 million raise exemplify capital flowing toward conflict-adjacent opportunities. Defense tech resurged as a focal point, driven by immediate security demands.

Life sciences suffered the most: only 23 new portfolio additions among Israeli VCs, down from 129 in 2022.

Israeli VC funds still hold approximately $11 billion in available capital—a war chest. The Israel Innovation Authority launched "Startup Fund" and "Yozma 2.0" initiatives to increase market liquidity, suggesting institutional recognition of opportunity amid crisis.

With larger rounds funding longer stealth periods, and defense/AI sectors attracting premium valuations, the ecosystem appears to be consolidating around geopolitical advantages. The question is whether Israel's innovation pipeline can maintain diversity while the world's attention—and money—fixates on its security innovations.