Israel’s Startup Squeeze Is a Warning for Dollar-Funded Tech Everywhere

AI is cutting the need for software labor just as the shekel is making Israeli labor more expensive.

Israel’s Startup Squeeze Is a Warning for Dollar-Funded Tech Everywhere

Venture capital likes to pretend software is borderless. Payroll is not. Israel’s startup economy has survived wars, recessions, political shocks and frozen capital markets. Its latest stress test is stranger: a strong shekel, a weak dollar, wartime disruption and AI arriving at the same time. Each would be manageable in isolation. Together, they are exposing a hidden weakness in the venture model: companies raise in dollars, spend in local currency and discover too late that macro can burn runway faster than bad management.

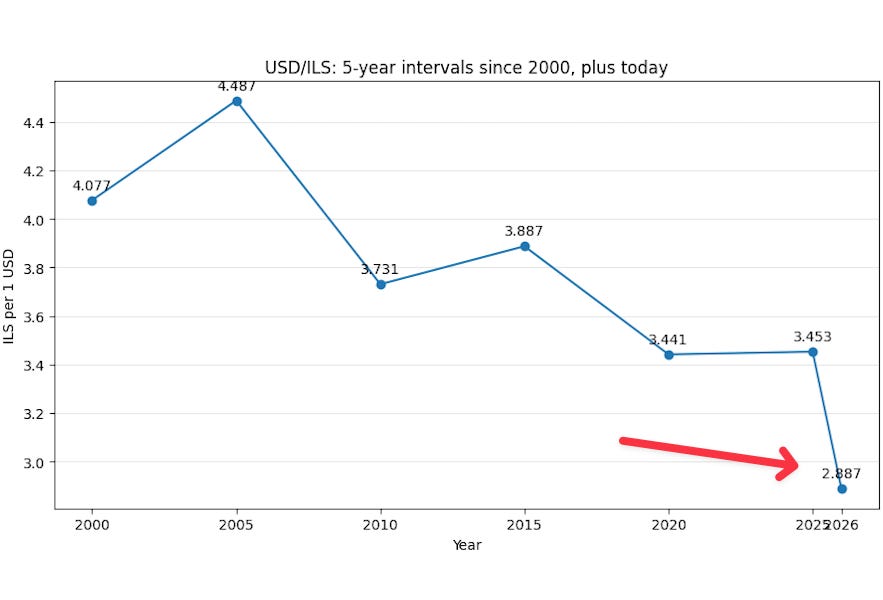

The dollar’s fall below NIS 2.90 this week is not a financial-market footnote. It goes directly into startup operating plans. A $10 million round that translated into roughly NIS 36 million when the dollar was near NIS 3.60 is worth less than NIS 29 million at NIS 2.887. Nothing fundamental inside the company changed. The product did not miss a milestone. The founders did not overhire. The investor deck did not overpromise any more than usual. Yet the company’s runway shrank by about 20%.

That is the kind of damage venture investors usually associate with execution failure. Here, it is currency translation.

The pain is concentrated where Israeli tech is most exposed: seed to Series C companies that are not yet cash-flow positive, raised in dollars, employ heavily in Israel and still need to hit milestones before raising again. Seed companies lose months of experimentation. Series A companies delay hires or narrow product scope. Series B and C companies face the uglier problem: their next round will be judged against stricter efficiency metrics while their shekel-denominated cost base has become more expensive in dollar terms.

For global investors, this is not just an Israel story. It is a portfolio-risk story. The same mismatch exists anywhere companies raise in dollars and spend in appreciating local currencies: Europe, India, Latin America, Singapore, parts of Eastern Europe. Venture capital has spent years pricing software as if capital, talent and customers existed in one clean global market. They do not. Revenue may be dollarized. Payroll remains stubbornly local.

Israel makes the problem impossible to ignore because the country’s tech sector is not ornamental. High-tech accounts for a disproportionate share of GDP, exports, tax receipts and foreign investment. When Israeli startups get squeezed, the issue is not merely founder discomfort. It becomes a question about one of the world’s most strategically important innovation clusters: cyber, defense, chips, AI infrastructure, enterprise software and the R&D networks of global technology companies.

The timing is brutal. Israeli tech employers were already under pressure from war, reserve duty, delayed sales cycles and skittish capital. Wages in Israel have reportedly jumped 15%-20% in dollar terms within months. The Israel Innovation Authority‘s wartime survey found that 62% of high-tech companies said the security situation hurt their ability to meet development or sales targets. A separate report said 71% of startups reported a fundraising hit from the war, and half could exhaust funds within six months.

Now add AI, the radical accelerant masquerading as a productivity tool. AI helps Israeli startups do more with fewer people. It can make two founders look like a twelve-person team. It compresses coding, design, testing, sales operations, customer support and internal analytics. For lean companies, that is survival technology. But AI also lowers the value of ordinary software labor. It forces investors to ask a harsher question: why finance expensive engineers in Tel Aviv building software that may soon become a feature inside a foundation model?

The shekel makes Israeli labor more expensive in dollar terms just as AI makes undifferentiated software labor less scarce. A strong engineering culture is still valuable, but it is no longer sufficient. In the previous era, “elite Israeli team attacking a large market” could clear a venture committee. Today, investors want proof of a moat: proprietary data, distribution, security urgency, deep technical advantage, regulated workflows, hardware integration or some defensible reason the product will not be eaten by OpenAI, Anthropic, Microsoft, Google or a better-capitalized competitor with cheaper labor.

Previous strong-shekel cycles had escape valves. Venture capital was more abundant. Global software demand was expanding. Multinationals were adding Israeli R&D capacity. Founders could hedge some dollars, defer hiring, trim burn and wait for the next round. Growth covered a lot of sins.

This cycle is less forgiving because the buffers are weaker. Capital is more selective. War has made operations unpredictable. AI has changed what investors think software companies are worth. The market is no longer paying equally for all forms of technical competence. It is separating strategic assets from expensive headcount.

That distinction matters. AI-native cyber, defense tech, data infrastructure, chips, robotics and deep-tech companies may benefit from urgency and scarcity. Their products are tied to hard problems, real budgets and geopolitical demand. Generic SaaS companies face the opposite reality. A workflow tool with no proprietary data, no distribution advantage and a high Israeli payroll is not a startup anymore. It is a currency-sensitive services business with venture branding.

The multinational angle is equally important. Israel has long been a premium R&D hub for global technology companies. That status will not disappear; the country’s technical depth, military-linked talent networks and cyber expertise remain difficult to replicate. But marginal hiring decisions are easier to move than national reputations. If the shekel stays strong and AI keeps compressing software output, global companies will ask which Israeli roles require proximity to elite talent and which can be shifted to cheaper hubs.

That does not mean Israel’s startup machine is breaking. It means it is being repriced.

The best companies will adapt quickly. They will hedge earlier, hire more selectively, push non-core roles abroad, use AI to reduce headcount, cut burn before investors force them to and sharpen their claims around defensibility. The weaker ones will discover that the old venture formula—raise dollars, hire aggressively, sell future growth—does not survive a stronger local currency, a war economy and a market that no longer rewards software for merely existing.

Israel is the acute case. The lesson is global. Venture investors spent the last decade underwriting growth and treating macro as background noise. Now FX, geopolitics and AI are moving into the cap table. In the next cycle, the question will not be whether a startup is in a hot market. It will be whether its cost base, currency exposure and technical moat can survive contact with reality.

Good piece.