Shekel On Steroids Squeezes Startups

AI is cutting the need for software labor just as the shekel is making Israeli labor more expensive.

Israel’s startup economy has survived wars, recessions, political shocks and frozen capital markets. It may now face a more perplexing test: a currency shock arriving at the same time as war fatigue and AI disruption.

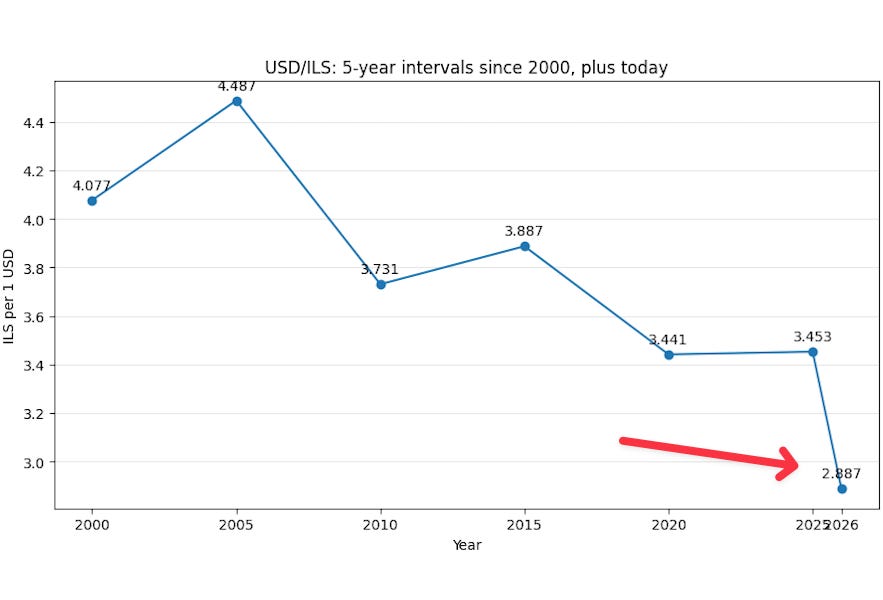

The dollar’s fall below NIS 2.90 is not just a macroeconomic curiosity. It cuts directly into the financial model of Israeli start-ups. Young Israeli companies typically raise capital in dollars, hire engineers in Israel and spend much of their budget in shekels. When the shekel strengthens, the same venture round buys less runway. A $10 million round that translated into about NIS 36 million when the dollar was around NIS 3.60 is worth less than NIS 29 million at NIS 2.887. The company has not hired recklessly. Its product may not have missed a milestone. But its operating life has shortened.

For seed to growth-stage software companies, the impact is immediate: fewer hires, shorter runway, tighter milestones and less room for error.

A stronger shekel does not hit all companies equally. It is most painful for seed to Series C companies that are not yet cash-flow positive, have Israeli-heavy payrolls and need to hit milestones before raising again. Seed companies lose months of runway. Series A companies delay hires or reduce product scope. Series B and C companies face a more strategic problem: the next investor round will be judged against tighter efficiency metrics, while their shekel-denominated cost base has risen in dollar terms.

All of this matters because Israeli technology is not just another export sector. High-tech accounts for a disproportionate share of Israel’s GDP, exports, tax receipts and foreign investment. The timing isn’t ideal.

Israeli tech employers are already under pressure. Within just a few months, wages in Israel have jumped by 15%-20% in dollar terms. The Innovation Authority’s wartime survey found that 62% of high-tech companies said the security situation hurt their ability to meet development or sales targets. A separate report said 71% of start-ups reported a fundraising hit from the war, and half could exhaust funds within six months.

Added to the mix is AI, and it cuts both ways. It can help Israeli startups do more with fewer people. It can make two founders look like a 12-person team. It can accelerate coding, sales operations, support, design and testing. But it also reduces the value of mediocre software. Why fund another software company with expensive engineers unless its product has some moat that AI cannot easily replicate?

In previous strong-shekel cycles, Israeli tech had escape valves. Venture capital was more abundant. Global software demand was expanding. Multinationals were adding Israeli R&D capacity. Founders could cut some costs, hedge some dollars, defer hiring and wait for the next round. The system adapted because growth covered mistakes.

This cycle could be less forgiving because all three buffers are weaker. Capital is more selective. War has made operating conditions less predictable. AI is changing what investors believe software companies are worth. A start-up cannot simply say it has strong engineers and a large market. It must now show why its product will not become a feature inside a foundation model, why its Israeli cost base is justified, and why its runway can survive both FX volatility and sustained reserve-duty disruption.

The strong shekel is not just a currency story. It is a stress test of the Israeli innovation engine. The best companies will adapt. AI-native cyber, defense, data infrastructure, chips, robotics and deep-tech companies may benefit from urgency and scarcity. Startups with vague SaaS tools, high Israeli payrolls and no clear AI moat will be repriced. Some will move hiring abroad. Some will hedge earlier. Some will cut before raising. Some will disappear without a headline.

Good piece.